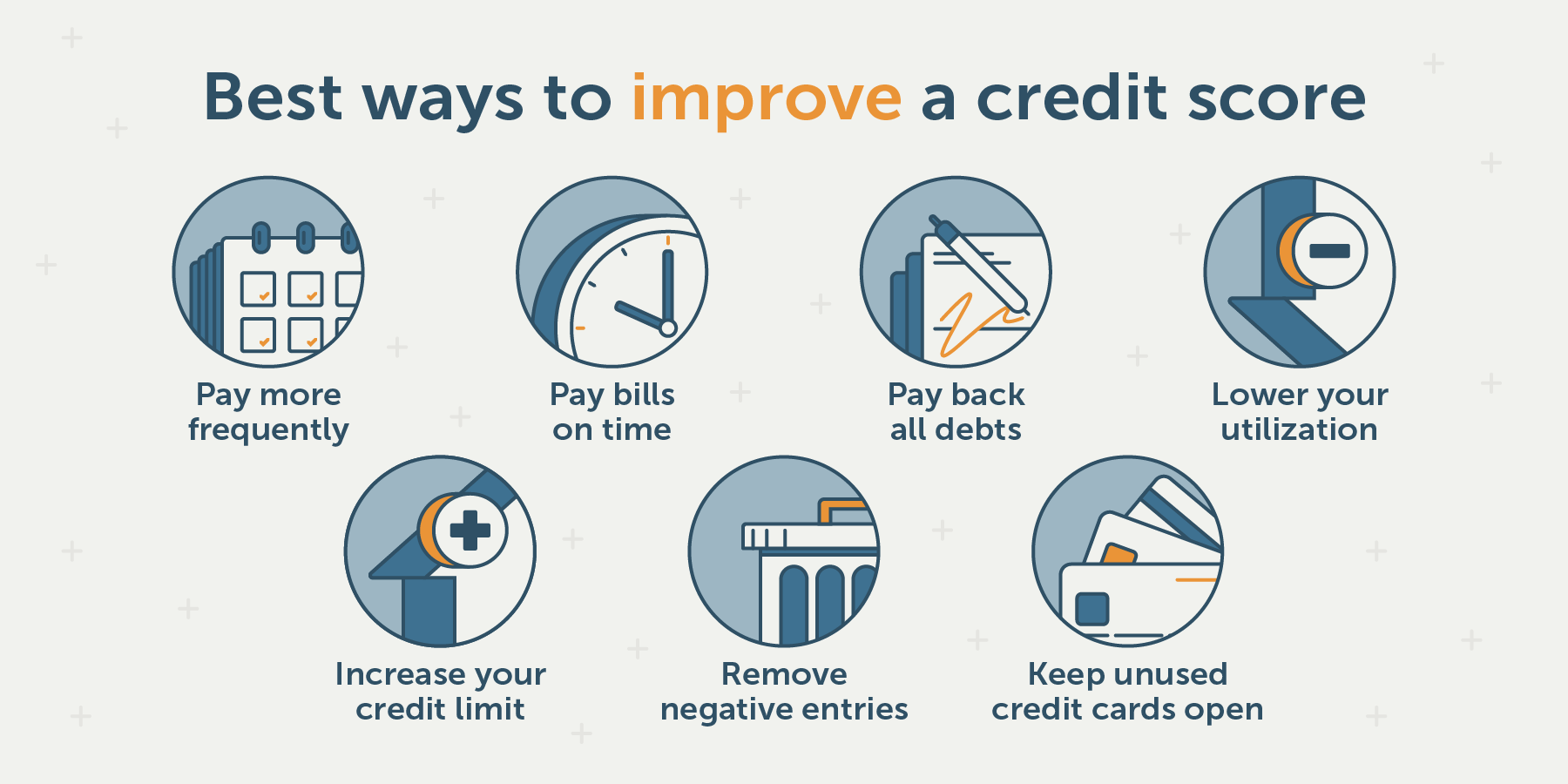

Opening a non-resident bank account in the UAE can feel like maneuvering through a complex maze. However, with the right guidance, you can simplify the process. You’ll need to understand eligibility requirements, types of accounts, and necessary documents. Each step is vital to guarantee a smooth application. So, what do you need to know to get started and avoid common pitfalls? Let’s explore the essential aspects of this banking journey.

Understanding Non-Resident Bank Accounts in the UAE

A non-resident bank account in the UAE is designed for individuals who live outside the country but wish to manage finances within it. These accounts offer several benefits, including easy access to funds, online banking services, and competitive interest rates. Understanding how these accounts work can help you make informed decisions about your banking needs in the UAE.

What is a Non-Resident Bank Account & Who Is It For?

Non-resident bank accounts in the UAE serve as an essential financial tool for individuals living outside the country but looking to manage their finances within its borders. These accounts offer non-resident benefits such as easy access to digital banking services, enabling one to handle their finances conveniently from anywhere. Non-resident accounts allow for efficient currency exchange, making it easier to transact in multiple currencies. They also help you navigate the complex banking regulations of the UAE while providing a secure platform for account management. Whether you are an expatriate, frequent traveler, or investor, a non-resident bank account can simplify your financial dealings and enhance your ability to manage assets in the UAE effectively.

Key Benefits: Why Open a UAE Account as a Non-Resident?

Opening a bank account in the UAE as a non-resident offers numerous advantages that can greatly enhance your financial management. First, you gain financial flexibility, allowing you to manage your assets efficiently across borders. With various currency options, you can hold accounts in multiple currencies, minimizing conversion fees. Online banking services provide you with easy access to your funds and enable seamless transactions, no matter where you are. Additionally, opening a UAE account opens doors to lucrative investment opportunities, letting you capitalize on the region’s growing economy. Furthermore, you’ll benefit from competitive fee structures, which can reduce your banking costs. Overall, a non-resident account in the UAE is a strategic move for your financial health.

Eligibility: Who Can Open an Account?

If you’re considering opening a non-resident bank account in the UAE, it’s crucial to understand the eligibility requirements. Various profiles, such as investors and international business owners, typically qualify for these accounts. Knowing these key facts can help you determine if you meet the criteria to start your banking journey in the UAE.

10 Key Facts About Qualifying as a Non-Resident

To qualify for a non-resident bank account in the UAE, you must meet specific criteria set by the banks. Generally, you’ll need to prove your non-resident status, which often requires documentation like a passport, proof of address, and a valid visa from your home country. Be aware of the tax implications that may arise from holding an account abroad, as your home country’s laws could affect you. Additionally, familiarize yourself with the banking regulations in the UAE to guarantee compliance. Most banks offer various options for currency exchange, allowing you to manage your funds effectively. Finally, prioritize account security by choosing institutions with robust security measures to protect your assets.

Common Profiles (Investors, Int’l Business Owners, etc.)

Many individuals and entities are eligible to open a non-resident bank account in the UAE, including investors, international business owners, and expatriates looking to manage their finances more effectively. Your investor motivations might include:

- Business expansion into the UAE market

- Access to diverse financial services tailored for international needs

- Flexible currency options for global transactions

- Steering through legal considerations to protect your assets

Types of Non-Resident Accounts Available

When considering a non-resident bank account in the UAE, it’s crucial to understand the types available to you. You can choose from savings and current accounts for everyday banking needs or opt for investment and wealth management accounts designed for more strategic financial growth. Each type offers unique benefits, so evaluate your financial goals to make the best choice.

Type 1: Savings & Current Accounts

Non-residents looking to open a bank account in the UAE typically have two main options: savings accounts and current accounts. Each serves different financial planning strategies and offers distinct features.

- Savings Accounts: Ideal for earning interest with competitive rates.

- Current Accounts: Perfect for everyday transactions and bill payments.

- Digital Banking Trends: Enjoy seamless online banking services for easy account management.

- Account Security Measures: Benefit from robust security features to protect your funds.

When choosing, consider factors like currency exchange rates and account accessibility. Both account types provide convenience and flexibility, making it easier for non-residents to manage their finances while living abroad.

Type 2: Investment & Wealth Management Accounts

After considering savings and current accounts, you might want to explore investment and wealth management accounts tailored for non-residents. These accounts provide you with the opportunity to implement investment strategies that align with your financial goals. They focus on wealth diversification, allowing you to spread risk across various assets while keeping an eye on market trends.

Effective risk assessment and portfolio management are essential components of these accounts, ensuring your investments are balanced and well-positioned for growth.

| Account Type | Key Features | Ideal For |

|---|---|---|

| Investment Account | Stocks, mutual funds | Growth-oriented investors |

| Wealth Management | Personalized financial advice | High-net-worth individuals |

| Retirement Account | Long-term investment options | Future financial security |

Non-Resident vs. Resident Accounts: 5 Key Differences

When choosing between a non-resident and a resident bank account in the UAE, it is crucial to understand the key differences that could impact your banking experience. You’ll find variations in fees, minimum balance requirements, and account features that cater to your specific needs. This comparison will help you make an informed decision as you set up your banking in the UAE.

A Quick-Comparison Table (Fees, Minimum Balance, Features)

Understanding the differences between non-resident and resident bank accounts in the UAE is essential for making the right choice for your financial needs. Here’s a quick comparison of key features:

- Fees: Non-resident accounts often have higher fees than resident accounts.

- Minimum Balance: Non-residents usually face higher minimum balance requirements.

- Digital Banking: Both accounts offer digital banking, but options may vary for non-residents.

- Currency Exchange: Non-resident accounts may offer limited currency exchange features compared to resident options.

When considering your account, think about account security, investment opportunities, and how banking regulations might affect your choices. By weighing these factors, you can make an informed decision that suits your lifestyle and financial goals.

Required Documents: Your Application Checklist

Before you start your application for a non-resident bank account in the UAE, you’ll need to gather some essential documents. This includes standard requirements like your passport and proof of address, along with bank-specific and source-of-income documents. Having everything ready will simplify the process and help you get your account set up efficiently.

Standard Document Requirements (Passport, Proof of Address, etc.)

To successfully open a non-resident bank account in the UAE, you’ll need to gather specific documents that verify your identity and address. These document types are essential for both identity confirmation and address verification during the application process, aligning with bank policies. Here’s a checklist to help you prepare:

- A valid passport (ensure it’s not expired)

- Recent utility bill or bank statement for address proof

- A passport-sized photograph

- Completed bank application form

Having these documents ready can simplify your experience and increase your chances of approval. Make sure all documents are clear and legible to facilitate a smooth application process. Happy banking!

Bank-Specific & Source-of-Income Documents

In addition to the standard documents required for opening a non-resident bank account in the UAE, you’ll also need to provide specific bank-related and source-of-income documents. Different banks may have varying requirements based on their regulations, so check with your chosen institution regarding account types and fee structures. Typically, you’ll need proof of income, such as payslips or tax returns, to demonstrate financial stability. If you’re looking to explore digital banking features or investment opportunities, some banks may request additional documentation. Be certain to gather all necessary documents to simplify your application process and guarantee compliance with bank regulations. Doing so will help you access the benefits of banking in the UAE efficiently.

How to Open Your Account: A 5-Step Process

Opening your non-resident bank account in the UAE is straightforward if you follow a clear process. You’ll need to choose the right bank, prepare your documents, and submit your application. Let’s break down the five essential steps to get your account up and running smoothly.

Step 1: Choose the Right Bank for Your Needs

Choosing the right bank for your non-resident account is essential, as it can greatly impact your banking experience in the UAE. Start by evaluating the various banking options available. Consider the following factors:

- Account types: Look for accounts that suit your financial goals, regardless of whether for savings or transactions.

- Fee structures: Compare monthly maintenance fees, transaction costs, and withdrawal limits.

- Digital banking: Confirm the bank offers robust online services for easy management of your finances.

- Investment opportunities: Check for options like mutual funds or fixed deposits that align with your investment strategy.

Step 2: Prepare & Notarize Your Documents

After selecting the right bank, the next step involves gathering and notarizing your documents. You’ll need to fulfill specific document requirements that typically include your passport, proof of residency, and a reference letter from your current bank. Make certain to check the bank’s website or contact them for detailed requirements. The notarization process is essential, as it guarantees your documents meet international standards and are legally recognized. Many banks offer online services to facilitate this process, but you may need to visit a local notary public. Keep in mind the legal implications of submitting improperly notarized documents, as they can delay your application or lead to rejection. Verify everything is in order to move forward smoothly.

Step 3: Submit Your Application (Online/In-Person)

Once you’ve gathered and notarized your documents, it’s time to submit your application, which can often be done online or in person, depending on the bank’s preferences.

During the application process, consider the following points:

- Online Submission: Conveniently upload your documents through the bank’s website.

- In-Person Requirements: Bring original documents and identification to your chosen branch.

- Application Tracking: Keep an eye on your application status via the bank’s portal or customer service.

- Document Verification: Confirm all documents are properly verified before submission to avoid delays.

Step 4: Pass the Initial Review & Compliance Check

To successfully open your non-resident bank account in the UAE, you’ll need to pass the initial review and compliance check, which is vital for guaranteeing that your application meets regulatory standards. This initial review process involves a thorough examination of your submitted documents against compliance requirements set by the bank and regulatory authorities. It’s important to verify that your documentation accuracy is impeccable, as any discrepancies can delay your application. The bank will conduct account verification steps to confirm your identity and financial background. Prepare for potential follow-up queries from the bank, as they may seek additional information to finalize your application. Meeting these compliance standards is key to progressing smoothly to the next step in opening your account.

Step 5: Fund and Activate Your Account

Now that you’ve successfully passed the initial review and compliance check, it’s time to fund and activate your non-resident bank account in the UAE. You’ll need to choose from various funding options available, such as wire transfers or deposits through international payment methods. Once your initial deposit is made, you can activate your account, giving you access to online banking features.

Consider these elements as you proceed:

- Transfer funds from your local bank

- Utilize currency exchange services if needed

- Set up online banking for easy access

- Confirm successful activation with the bank

Completing these steps will guarantee your account is fully operational, allowing you to manage your finances efficiently from abroad.

Top UAE Banks for Non-Residents: A Quick Comparison

When considering a non-resident bank account in the UAE, it’s crucial to compare the top banks based on key features, minimum balances, and their respective pros and cons. Each bank offers unique benefits that can cater to your financial needs. In this section, we’ll break down what you should know to make an informed choice.

Key Features, Minimum Balances, and Pros & Cons

Steering through the landscape of banking options for non-residents in the UAE can be straightforward if you understand the key features, minimum balance requirements, and the pros and cons of different banks. Here’s what to evaluate:

- Account types: Various options, including savings and current accounts.

- Minimum balances: Typically range from AED 3,000 to AED 10,000, depending on the bank.

- Banking benefits: Access to international wire transfers and online banking facilities.

- Pros & cons: Benefits include easy access to funds, while cons may include higher fees for lower balances.